The Difference Between a Line and a Curve

Why software, venture, and a lot of careers are all about to get sorted

A few months ago I argued that the greatest business model of the last twenty years was breaking. Enterprise SaaS, the seemingly bottomless gold mine, finally running into math it could not out-grow. A lot of people read it. Almost nobody asked the obvious follow-up…

You’ll see why further down, but the reaction from nearly everyone was “OK, so what’s the next shiny object we should be chasing after?” And therein lies the problem.

Okay. So what actually happens next?

Not to the model. To the companies living inside it. To the people whose job is to price them, fund them, and predict them. That is the part I left on the table, and it is the part that actually matters, because diagnosis is cheap right now. Everyone can see the multiples compressing. Everyone can recite the AI margin story. What almost nobody is doing is the harder thing, which is figuring out where the curve goes from here, who gets hurt on the way and how the safe space is a moving target.

I have been making one version of this argument for a long time. My very first post, ten years ago, was about why a one percent cut to revenue guidance could take a stock down forty percent. The answer was that the cut runs through the income statement once and then compounds every quarter, so a tiny change in the slope produces a violent change in the destination. I called it taking a double derivative. My instinct was right, and it is the whole game here too, even though I initially called it too early and without a clear why.

SaaS has always been about the derivative. The slope of the curve we are on. Where we are matters far less than where we are headed, and you cannot read where you are headed off just the position. You read it off the rate of change, and then the rate of change of the rate of change, which is where things get genuinely weird. Discussing ARR at all without this context is borderline irresponsible.

Most people are only reacting to the position. The position is the weakest seat at the table. So let us do the other thing.

The two forces, and the double whammy

Start with what makes any business great. It needs to be two things at once. It needs to be unique, which is what lets you set your price, and it needs to be compelling, which is what guarantees someone shows up to pay for it. Unique drives the pricing. Compelling drives the volume of dollars. Simple enough. (This is derived from a concept I heard in a Pat Grady interview).

A great example of a product that is both unique and compelling is the Bloomberg Terminal. For traders on Wall Street, it is the enabling layer to efficiently get the job done (compelling), and it is the only game in town (unique, with network effects as moat to maintain that position). The result is almost unbounded pricing leverage and continued growth. It also helps that they sell into a highly profitable sector.

Here is what people miss: these are not two independent dials. They are coupled. When uniqueness fades, you do not just lose pricing power and keep your demand. You eventually lose both, because a thing that anyone can make is a thing that everyone makes, and a thing that everyone makes is no longer something people are desperate to buy from you specifically (or anyone else for that matter).

So when uniqueness goes, you get eaten from the top and the bottom at the same time. Pricing compresses while the cost of winning and keeping each customer climbs. That is the double whammy, and it is nastier than either problem alone, because the standard tools show you the two halves on different lines of the page and let you pretend they are unrelated. They are not unrelated. They are the same event with different symptoms.

A word about that word: Contribution Margin

This is where I have to slow down, because the moment a business starts struggling, everyone reaches for a more sophisticated piece of vocabulary, and right now the fashionable one is contribution margin. People say it the way they used to say total addressable market, as if saying it is the same as understanding it.

It is not. And reaching for the term without earning it is more dangerous than never reaching for it at all.

Here is why the term exists. A normal income statement was built for a normal business, one that buys materials, makes a thing, and sells it. Revenue and cost of goods at the top, then the operating cost lines below, and by the time you reach the bottom you have a clean read on the health of the operation. Software broke that read. The cost of delivering one more copy of the software is basically nothing, so gross margin looks gorgeous forever. But the cost of getting and keeping each customer is not nothing, and it is not fixed, and it is not a one-time investment in growth. It is a recurring, variable cost of simply existing. And it has been very easy, entirely within the rules, to let that cost hide inside the S&M line and the R&D line, where it reads like ambition instead of like the cost of staying alive.

Nobody is breaking accounting rules. The rules just were not built to describe this kind of business, so we use translation hacks which quietly mislead, and the misleading compounds.

Contribution margin is the term we invented to drag that hidden cost back into the light. Fine. But if you do not understand the accounting it is correcting, if you do not understand why the standard picture lies in this specific way, then you have not actually diagnosed anything when you say the words “contribution margin”. You have just renamed the excel row and felt smart. You imported the vocabulary without importing the comprehension that makes the vocabulary mean something, and that gives you a false sense that you have double-clicked when all you did was learn a phrase.

(This is unfortunately not dissimilar to every founder doing a Find/Replace with “Revenue” for “ARR” without actually understanding that no, their ice cream parlor does not have “ARR”).

I am not being pedantic for sport. This is the entire failure mode of the last decade, and it shows up everywhere once you see it.

The metrics stopped meaning what you think they mean

Take the holy SaaS unit economics ratio, LTV:CAC. For years it was the number. Healthy ratio, pour in more money, watch it grow. The problem with optimizing around a compound metric is that it bundles a dozen assumptions into one clean-looking number, and when the driving assumptions underneath get stripped away, the number does not tell you. It just sits there looking healthy while the thing it was supposed to measure rots. Simply put: it’s way too easy to manipulate - both by accident and on purpose.

So you cannot diagnose one of these businesses from a single snapshot. You cannot even do it from a few snapshots strung together, the seed numbers, then the Series A numbers, then the Series B. That gives you a few points, and a few points let you draw a line, and a line is exactly the thing that will fool you. To actually understand the business you have to get into the definitions sitting inside the BI tools, the precise meaning of every variable, and then take the second and third and fourth derivatives of each one, because that is where the shape goes strange. Every variable in a business can bend like that. Combine a few of them bending at once and it gets very hard to hold in your head, and arguably even harder to calculate in a spreadsheet.

This is the reason leading VC voices have bounced between “this metric matters the most now!” 10 times in just as many years. It’s reactionary, it’s not clever or deep.

I have been hating on “net churn” since I first heard it in an investment committee meeting in 2014. I also hated its rebrand: net dollar retention (which when calculated a simple number is exactly the same meaningless vanity metric).

It is so much easier to grab a metric, assume it holds, and move on. For a long time you could get away with that, longer than I expected, honestly. But the assumptions were always doing the real work, and when they go, the metric is the last thing to admit it.

We did two things when I was banker:

We invented metrics that we thought aptly described a business and would make it seem compelling to the market.

We benchmarked metrics which companies disclosed at IPO and then in every subsequent quarters’ financial reports.

At the time, these felt like a similar idea, when in fact they were coming from very different places. Mode 1 wants to market, sell and get deals done. It’s smart, but doesn’t think long term. It is exactly why Charlie Munger diagnosed VCs as becoming a lot like investment bankers. Works well for sell-side M&A, much tougher in the IPO game. Mode 2 is the venerable CFO in the room: “Once we tell Wall Street this number, they’re never going to stop asking for it. If we decline to share it, they will assume it cratered and they will sell. Let’s make sure we have a great handle on what this will look like in 5 years before we go advertising it as the key way to know if our business is working or not.”

The people reading the curve forgot how to read curves

Which brings me to the part nobody wants to say out loud.

It used to take about ten years to become a real general partner at a real VC fund. Not because it takes ten years to learn how to wire money or sit on a board or attract LPs with an exciting story about access or the ability to woo the next hot founder. Because it takes about that long to live through enough company cycles to see curves instead of lines. Ten years of board meetings, each one revealing something at a higher order than the last, and you slowly learn to string those meta-observations together into a feel for where a curve actually bends. That feel was the job. That was the skill the apprenticeship existed to build. As I look back on my time in board meetings with Harry Weller and Peter Barris, I can increasingly appreciate that they were playing 4D chess while others were playing checkers. That doesn’t mean they were always right, but they were doing a different job than what I see now. They were using thousands of data points to predict rather than just reacting to what they saw that day.

That apprenticeship has been compressed to months. Assets under management exploded, headcount exploded to match, and the comp-able skill stopped being judgment and became winning. Getting into the hot deal. Closing. Which tells you everything about supply and demand in this market. By the way, that the prized competence is access rather than discernment. And what’s a “hot deal”? It’s two points that make a steep line - at any stage in the business.

I want to be careful here, because the easy move is to mock the young VC, and that is both lazy and wrong. They are not dumb. They were trained in a regime where the shortcut worked. Two points, draw the line, if it is steep enough then go - fast. You can dress this up a million ways, but after 3 years of experience, there isn’t much else behind it. In an era of cheap capital and insatiable demand, that shortcut was not stupid, it was the rational adaptation. The market paid for it. The de-skilling is not a personal failing. It is what happens when an environment stops rewarding the slow thing and starts rewarding the fast one.

The trouble is that the environment changed and the trained reflex did not. You now have a lot of capital being steered by people who can read a line beautifully and have never been taught to read a curve, at the exact moment the curves got weird. That is the new variable this cycle. The forces underneath are the same as they always were. What is different is that the readers lost the training right when the reading got hard.

The result: while one would expect a massive influx of capital into a market to be distributed across that market, what has happened instead is the most aggressive concentration of capital in any market anywhere. The behavior of the human capital layer (i.e. VCs) in between the companies and the capital sources is the only explanation for this economic abnormality.

Where it actually goes

So let’s run the equations forward instead of reacting to where they sit today. This exercise is harder today than it has been in the last 20 years, but it’s still worthwhile.

Uniqueness keeps decaying, because building keeps getting easier and everyone keeps aiming at the same problems. Pricing power keeps leaking. The cost of selling into a crowded category keeps climbing. The compound metrics keep flattering everyone until they suddenly do not. None of this points to a dramatic collapse. It points somewhere more boring and more certain. It points to software becoming a commodity utility. Genuinely needed, deeply embedded, and priced like plumbing, because nobody pays a premium for the ninth-best version of a thing they can no longer tell apart from the other eight. If you’re already embedded, great. If you think you’ll unseat someone by being “twice as good” (whatever that means), then good luck.

This is the larger pattern, and it is older than software. Everything interesting starts as a cottage. In the cottage phase the learnings come fast and the margins are fat, precisely because the thing is not yet legible, not yet crowded, not yet systematized. Being early to something illegible is the whole reason the returns are so good. Then it industrializes. And industrialization is exactly the process that flattens the curve. The learnings slow, the margins thin, the talent rushes in, the second derivative drifts to zero, and what was a beautiful arc settles into a straight, unremarkable line. That is not a tragedy. It is the maturation signature of every field that ever worked. SaaS just lived a particularly glorious version of it. Faster and more scalable than anything else that came before it.

For anyone who has watched a cottage become an industry before, none of this is jarring. It is a natural progression, and the panic in the room is mostly coming from people who have only ever seen the cottage.

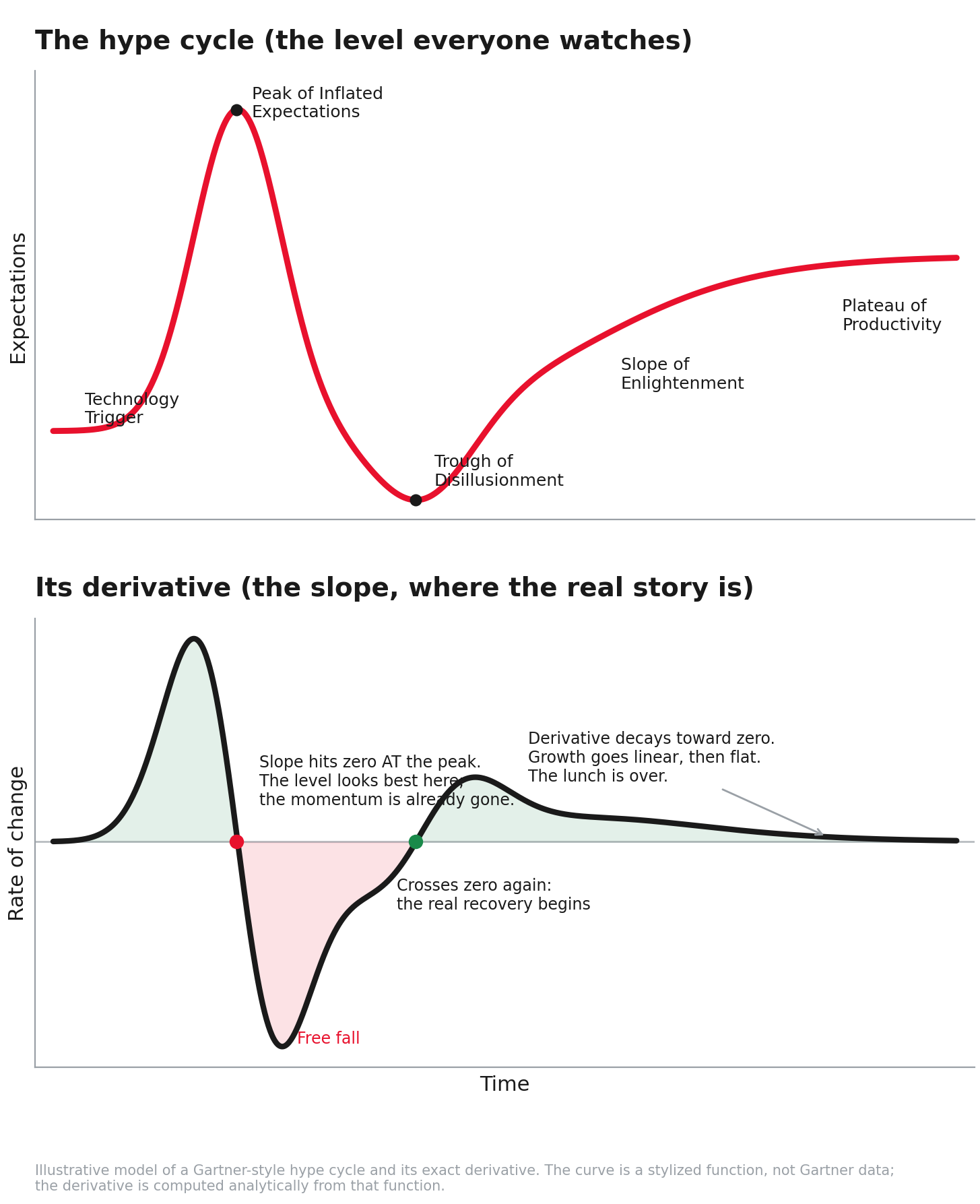

The Gartner Hype Cycle actually maps very well to this… with one major modification. The Hype Cycle describes our position, but if we want to know where we’re headed, we need to take a derivative. They were nice enough to draw a line and we can infer its slope at every point on that line, thus understanding what actually matters in an always forward looking market: where it’s going.

Enter the Derivative of the Hype Cycle:

A natural transition, and who it runs over

Not the sector. The sector is fine. It is becoming infrastructure, and infrastructure is a perfectly good thing to be.

You can watch this happening right now, one layer up the stack. The frontier AI labs were supposed to be the purest cottage on earth, the most illegible, fastest-learning, fattest-margin thing anyone had ever seen. And yet the cleanest money in that arena today is not a model winning on being unique and compelling. It is rent on the data center. Labs that could not differentiate the product are leasing out the compute underneath it, to their own direct competitors, on multi-year contracts worth more than the product itself has ever earned. That is not a frontier lab. That is a landlord. The cottage industrialized into infrastructure in about eighteen months, and the value slid down the stack from the curve to the asset while everyone was still arguing about the model.

Which is the whole asset management story in one move. The model was a venture bet on a curve. The data center is a private equity asset, financeable, depreciating, underwritten on a contracted cash flow with almost no room for error. When the value moves from the model to the building, the natural owner moves with it, from the VC to the buyout shop to the infrastructure credit desk. Returns get smaller and more predictable, leverage becomes an earned privilege, and the diligence gets rigorous because there is no convexity left to forgive a miss. The instrument has to match the curvature, and here you can watch it matching in real time.

The collateral damage is specific. It is the companies approaching linear growth while still running the grow-or-die playbook which was force fed to them half a cycle ago. The ones who mistook the industrial phase for the cottage phase and kept pricing and spending and hiring as if the learnings were still free and the margins were still fat. The regime quietly switched underneath them. Grow-or-die became survive to be profitable, and a lot of companies are still optimizing for a game that ended. Cultural shifts are often the most uncomfortable but remain an unavoidable evolution in every market.

The skills that allow you to reach profitability are the same ones that allow you to grow as fast as possible. It’s about efficiency. Having your hands on the levers and a deep understanding of the interdependencies is how you control your destiny.

That is the now-what. Not a crash. A regime change, and a sorting, where the businesses that can flip into sustainability live and the ones built entirely around a slope that no longer exists do not.

Capital structures will change. Many people will learn the hard way. But that is all part of a scaffolding coming down which was never meant to bear the weight of an industry growing and maturing on top of cottage infrastructure.

The other casualty is the same as with every other economic cycle: the people who thought that their point-in-time money machine hack would last forever, and instead of saving their outsized earnings, they let their inflated egos take credit for their earnings rather than a temporary market dislocation and were left instead with some amazing Instagram posts and $0 in diversified savings and/or way too little time spent with loved ones while they hustled towards a mirage.

The part that is actually about you

There is no free lunch in any of this, and there never was. The fat margin of the SaaS era was not free money. It was payment for being early to something illegible, and you do not get to keep collecting that payment once the thing is legible to everyone. The premium was rent on scarcity, and scarcity is a cottage property. The moment a thing industrializes, the rent compresses to a wage.

But the rent does not disappear. It moves. It relocates to whatever is still scarce, usually whatever stays hardest to build, copy, or learn. When the product commoditizes, the value slides to the asset underneath it (you just watched a frontier lab turn into a landlord). The rent did not die. It changed address.

This is true of a business model, and it is just as true of a skill, which is the uncomfortable part. The outsized reward for anything you can do is rent on how scarce it is. When your edge becomes teachable, hireable, or automatable, it industrializes, the rent on it compresses, and you feel that compression as the floor moving under you. The judgment that used to take ten years to build is industrializing right now. So is a great deal of what any of us do for a living.

So when the curve under you flattens, the rent on your edge relocates too, and you have two honest ways to follow it. The one you reach for tells you what your edge actually was the whole time.

You can go find another illegible thing. Another cottage, another curve with curvature still in it, where the learnings are fast and nobody can tell you yet whether it will work. If that is the move you reach for, your edge was the reading. The craft of pricing the illegible, wherever it happens to live. You pay for that edge in uncertainty, up front, every time, and the cost is real even when it does not look like a cost on the way in.

Or you can stay exactly where you are and change your instrument. Keep the market you know cold, the one that just grew up, and trade the tool it rewards now for the tool it rewarded when it was young. If that is the move you reach for, your edge was never the tool. It was the market, and the reading was just the costume that market handed you while it was still a cottage.

That second move is not a retreat, and it is not the lesser path. It is expertise figuring out where it actually lives. It is also exactly what the venture capitalists turning into private equity are telling you, if you listen past the spin. They did not lose the skill. They learned the skill was never venture. It was the market, and venture was only the instrument the early innings rewarded.

This is what my friend Isaac Heller means when he says it is better to pick the right table than to be good at poker. The table is the market. The poker is the instrument. Most people assume their whole career that they are simply good at poker, and never find out it was the table all along until the game at their table changes and they have to choose: learn a new game, or go find a new table.

The only one who gets hurt is the one who does neither. Who stays at a grown-up table still playing the cottage game, still pricing for a curvature that already left, still telling the old story to whoever will fund it. Which is just the company running grow-or-die a half cycle too long, one scale up. A person instead of a balance sheet, but the same error, and the same ending.

Which is just the derivative again, one more time. The money and the learning both live in the rate of change, not the position. The moment something goes linear, the lunch is over for everyone who showed up late. The whole trick, in a business or a career, is to be reading the curve while everyone else is still admiring the line.

P.S. We’ll get into the tactics of investment thesis formation and execution strategies in future pieces - both here and in the Verissimo Substack.

The frontier lab turning into a landlord is the observation that should restructure every AI investment thesis in the room. Eighteen months from cottage to infrastructure. The model was supposed to be the product. It became the marketing material for the compute lease underneath it. When a lab makes more from renting out the GPUs than from selling the model running on them, the value has already slid from the curve to the asset, and the natural owner slid with it, from the VC to the credit desk.

The apprenticeship section hits harder than the SaaS parts because it names the mechanism behind every deskilling story in every industry right now. The skill that took ten years was never "venture." It was watching enough cycles to see curves instead of lines. Compress the apprenticeship to months and you get people who can read a steep line beautifully and have never seen one bend. That works until the bend arrives, and the bend always arrives. The de-skilling isn't a generation problem. It's what happens every time an environment rewards speed over judgment long enough that the people it trained genuinely believe speed was the skill.

Great article, the SaaS era really was a blip on the historical timeline perhaps, a short lived anomaly that dragged crazy capital into venture under the illusion it was normalcy. The "correction" is less dramatic and more like a gradual return to baseline, where venture goes back to being real adventure capital and the easy money finds its way toward vehicles better suited to carry it. New debt structures and forms of collateral emerging around hard assets are genuinely creative and where good returns can get made. Curves getting harder to read as a return to normalcy.